PreferredProperties.Com - Real Estate Tips & Market Insights

The Influence of Wealth Concentration on US Housing Affordability and Availability

The increasing wealth gap in the United States, exemplified by the statistic that the top 1% of Americans possess sufficient wealth to theoretically purchase the vast majority of US homes, has profound implications for housing affordability and availability for the average buyer. This report analyzes the intricate relationship between this wealth concentration and the challenges faced by many Americans in securing adequate housing. The significant accumulation of wealth at the top not only distorts the housing market through increased purchasing power and investment activities but also exacerbates the divide between homeowners and renters, hindering social mobility. Understanding these mechanisms is crucial for policymakers seeking to address the growing housing crisis and promote a more equitable housing market.

3/18/202515 min read

The Growing Divide: Understanding Wealth Concentration in the US:

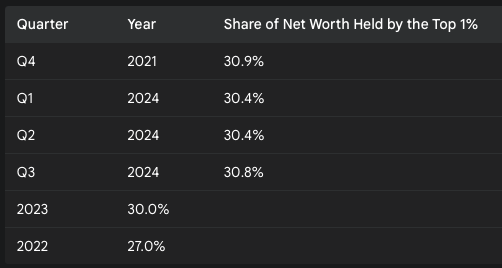

The distribution of wealth in the United States reveals a significant concentration at the very top. Data from the third quarter of 2024 indicate that the wealthiest 1% of the population held 30.8% of the nation's aggregate net worth . This substantial share signifies that a small fraction of households controls a disproportionate amount of the country's financial resources, potentially influencing various sectors, including the housing market. Looking back to 2023, this same group owned 30% of the net worth, a notable increase from the 22.8% recorded in 1990 . This upward trajectory over the past few decades illustrates a clear trend of increasing wealth concentration, although there was a slight decrease from the peak of 30.9% observed in 2021 . This recent fluctuation warrants attention to understand its causes and whether it signals a change in the long-term pattern.

The disparity becomes even more apparent when comparing the wealth of the top 1% to that of the bottom half of the population. As of the fourth quarter of 2021, the top 1% held 30.9% of the nation's wealth, while the bottom 50% held a mere 2.6% . This stark contrast underscores the extreme inequality in wealth distribution, with the wealthiest 1% possessing over ten times the wealth of the entire bottom 50%. Data from 2022, provided by the Congressional Budget Office (CBO), also confirm this trend, showing the top 1% holding 27% of total wealth, an increase from 23% in 1989 . While this figure is slightly lower than other reported percentages for similar periods, it consistently points to a substantial and growing concentration of wealth at the top.

Historically, this concentration has been on the rise. From 1989 to 2019, wealth became increasingly concentrated in the top 1% and the top 10%, partly attributed to the concentration of corporate stock ownership within these segments of the population . This suggests that ownership of corporate assets plays a significant role in driving wealth inequality, as gains in the stock market disproportionately benefit those at the higher end of the wealth distribution. Furthermore, the average wealth of individuals in the top 1% is more than a thousand times greater than that of people in the bottom 50% . This staggering ratio emphasizes the sheer magnitude of the wealth gap and the vast difference in financial resources between these groups. By late 2022, the total wealth held by the top 1% amounted to $43.45 trillion , a concrete figure highlighting the immense financial power concentrated within this small segment of the US population.

To illustrate the recent trends in wealth concentration, the following table summarizes the share of net worth held by the top 1% in the United States:

This data underscores the persistent and significant concentration of wealth within the top 1% of American households.

The Squeeze on the Average Buyer: The State of Housing Affordability and Availability:

The significant wealth concentration discussed above has a direct impact on the ability of average Americans to afford and access housing. In 2024, nearly half (49%) of all US households could not afford to purchase a home priced at $250,000 . This indicates that a substantial portion of the population is priced out of even relatively affordable housing options. The challenge becomes even more pronounced when considering the median price of a new single-family home, which stood at $495,750 in 2024. A staggering 77% of US households could not afford a home at this price point, based on prevailing mortgage rates . This demonstrates that the majority of households are unable to afford a typical new home, highlighting a significant affordability crisis.

The median sale price of existing homes also reached record levels in 2024, peaking at $442,000 in July . This continuous upward trend in housing prices makes it increasingly difficult for average buyers to enter the market. Indeed, housing affordability was identified as a growing crisis in 2024, particularly affecting lower-income groups . This suggests that those least able to afford housing are facing the most severe challenges, potentially leading to increased housing insecurity.

Compounding the affordability issue is the limited availability of housing. As of the third quarter of 2024, the national housing shortage was estimated to be 3.7 million units . This significant deficit in the number of homes available compared to the demand contributes to higher prices due to limited supply. While new home sales in September 2024 reached 738,000, exceeding the pre-pandemic average , this level of construction may not be sufficient to fully address the existing shortage or cater to the affordability needs of the average buyer. Similarly, existing home sales in November 2024 showed an increase to an annual rate of 4.15 million, the highest since March, but still below the figures from 2023 . This suggests that while there might be some improvement in sales volume, overall market activity remains constrained compared to previous years.

Furthermore, housing inventory, despite some increases, remained below historical averages throughout 2024 . This scarcity of available homes puts upward pressure on prices, further exacerbating the affordability challenges for potential buyers. High mortgage rates, fluctuating between 6% and 8% throughout 2024, also acted as a deterrent for many potential buyers, significantly increasing the overall cost of purchasing a home . In the multi-family housing sector, while completions have risen, the number of new construction starts has fallen sharply . This could impact the future supply of rental units. Notably, the national rental housing market experienced a relatively high vacancy rate of 8.9% in 2023 . While a higher vacancy rate might typically suggest downward pressure on rents, the underlying reasons and the extent to which this translates to more affordable rents in the long term require further consideration.

The Mechanism of Influence: How Wealth Inequality Impacts Housing Affordability:

The concentration of wealth in the hands of the top 1% exerts a significant influence on housing affordability through several key mechanisms. Their substantial purchasing power allows them to compete for and often acquire properties that are beyond the financial reach of the average buyer. By the end of 2024, the top 1% held a combined net worth of $49.2 trillion, a figure nearly equivalent to the total value of almost 100 million US homes, estimated at $49.7 trillion . This stark comparison, while theoretical, illustrates the immense potential for this small segment of the population to absorb a vast portion of the housing stock, thereby influencing market dynamics and pricing. Even within this elite group, the top 0.1% possesses enough wealth to purchase every home in the 25 most populous metropolitan areas , highlighting the concentrated buying power at the very apex of the wealth distribution, particularly in high-demand urban markets where affordability is already a major concern. Moreover, many wealthy individuals often purchase homes with cash, providing them with a significant advantage over buyers who require mortgages . Cash offers eliminate the contingencies and delays associated with financing, making them more attractive to sellers, especially in competitive markets, and further disadvantaging average buyers.

The increasing involvement of large institutional investors, often backed by billionaire wealth, also plays a crucial role in shaping housing affordability. These investors frequently treat housing as a commodity for speculation, aiming to extract increasing rents and value from multi-family rentals, single-family homes, and mobile home park communities . This shift in perspective, from housing as a fundamental need to housing as an investment asset, can lead to practices that drive up prices and reduce affordability for average buyers. Wealthy investors may acquire properties and hold them vacant, not to rent them out, but to profit from real estate appreciation . This practice removes units from the market, reducing the available housing stock and contributing to higher prices without addressing the immediate housing needs of communities. Furthermore, global billionaires invest billions in US real estate as a means of diversifying their asset holdings, often fueling the development of luxury housing . This focus on high-end properties can divert resources and development efforts away from more affordable housing options, exacerbating the supply shortage at lower price points.

The widening income and wealth gap has a direct and significant effect on housing affordability. Research indicates that income inequality increases housing costs as a share of income, making it more challenging for average earners to afford housing . As income inequality rises, wealthier individuals have a greater willingness to pay for houses, leading to increased demand and subsequently pushing prices upward . This competitive bidding process, driven by those with greater financial resources, makes it increasingly difficult for average buyers with limited budgets to compete effectively in the housing market. The expectation of continued house price appreciation, fueled by demand from wealthier individuals and investors, can also incentivize existing homeowners and investors to hold onto their properties rather than selling, further restricting the supply of available homes and maintaining upward pressure on prices . This creates a cyclical relationship where wealth concentration contributes to higher prices and reduced availability, making it even harder for the average buyer to enter the housing market.

Beyond Affordability: The Impact on Housing Availability for the Average Buyer:

The concentration of wealth not only affects the price of housing but also influences the type and location of housing available to the average buyer. Billionaire investors and their backed entities often prioritize the development of increasingly high-end properties, as these tend to offer higher returns on investment . This focus on luxury development can lead to a situation where the overall supply of housing might increase, but the availability of units affordable to the average buyer lags significantly. In fact, some analyses suggest that there is already a sufficient, and even an excess, of housing for the wealthy, while a critical shortage persists for housing priced at rates affordable to low-income households . This structural imbalance in the housing market indicates that the needs of different income segments are not being met equitably, potentially representing a market failure driven, in part, by the concentration of wealth and the incentives it creates for developers.

The impact of wealth concentration on housing availability also manifests in geographic disparities. Rising house prices, often driven by demand from wealthier individuals and investors, can lead to a concentration of wealth in metropolitan areas . This can make it exceedingly difficult for average-income individuals and families to afford housing in these economically vibrant regions, potentially limiting their access to job opportunities, education, and other amenities. As a result, individuals may be forced to seek housing in more affordable, but potentially less opportunity-rich, areas. The extreme income inequality observed in areas like the Jackson, WY-ID metro area and Teton County, WY , likely translates to similarly extreme challenges in housing affordability and availability for those outside the top 1%. In such areas, the immense wealth of a small percentage of the population can effectively price out the vast majority of residents.

Furthermore, the increasing prevalence of short-term rentals, often facilitated by platforms like Airbnb and Vrbo, and the investment in these properties by wealthy individuals and corporations, can also reduce the availability of homes for long-term residents . By converting residential properties into short-term rentals, investors can often generate higher returns through tourism. However, this practice decreases the supply of homes available for local residents seeking long-term housing, further impacting affordability and availability, especially in popular tourist destinations and urban centers.

The Widening Gulf: Consequences for Homeowners vs. Renters and Social Mobility:

The increasing wealth gap has significant consequences for the wealth disparity between homeowners and renters and for overall social mobility in the United States. Data from 2022 reveal that the median wealth gap between homeowners and renters reached a historic high of almost $390,000 . This demonstrates that homeownership has become a crucial driver of wealth accumulation, leaving those who are unable to afford to buy a home further behind in terms of wealth. The average wealth gap between these two groups was even more staggering, reaching over $1,370,000 in the same year . The significantly larger average gap compared to the median suggests that the wealth of homeowners is skewed towards the very top of the distribution, further emphasizing the extent of the disparity.

Recent gains in housing wealth are largely responsible for driving these median wealth disparities between homeowners and renters . Due to supply shortages and rising home prices, those who were able to access and sustain homeownership have experienced significant wealth accumulation through home equity. Conversely, renters face a higher housing cost burden, with a record high share spending more than 30% of their income on rent in 2022 . This leaves renters with limited residual income for saving and investment, preventing them from benefiting from the growth in financial markets and further widening the wealth gap.

The current housing market dynamics, influenced by wealth concentration, also pose significant challenges to social mobility. Rising house prices relative to incomes have made it increasingly difficult for individuals to save enough from their earnings to afford a down payment and purchase a home, particularly for those with lower incomes and without existing family wealth to provide support . This suggests that access to homeownership, a key pathway to wealth building and upward mobility, is becoming increasingly dependent on pre-existing family wealth, limiting opportunities for those from less affluent backgrounds . The fact that inheritances and family support are playing a growing role in enabling first-time home purchases reinforces this trend.

Research has also highlighted the racial dimension of this issue. Housing market appreciation between 1984 and 2021 is estimated to explain approximately 70% of the increase in the median White-Black wealth gap . This indicates that the unequal distribution of homeownership and the differences in housing values and returns between racial groups have significantly contributed to the widening racial wealth gap. Furthermore, studies suggest that relative wealth mobility is slower than earnings mobility, and that families with larger wealth stocks experience greater relative earnings mobility . This underscores the crucial role that wealth plays in determining economic mobility, and how the lack of wealth can exacerbate existing inequalities. The finding that bequest recipients are more likely to pursue self-employment and own a home further illustrates how wealth can expand opportunities and enhance social and economic mobility .

Navigating the Challenges: Policy Considerations and Potential Solutions:

Addressing the challenges posed by wealth concentration on housing affordability and availability requires a multifaceted approach involving various policy interventions. A critical area for focus is boosting the supply of housing across different price points. Increasing housing construction is essential to alleviate supply shortages and moderate price increases, which can help to narrow the housing and financial wealth gaps between homeowners and renters . Reforming zoning and land use regulations that often hinder new housing construction is also crucial . By allowing for denser and more diverse housing options, such as townhouses, duplexes, and apartments, communities can increase the supply of available and potentially more affordable housing. Direct federal funding to state and local governments can also play a vital role in supporting the construction of rental and homeownership units that are affordable to low- and moderate-income families .

To directly address affordability challenges, expanding rental assistance programs like Housing Choice Vouchers is essential . These subsidies help low-income households afford market-rate rents, alleviating their housing cost burdens and providing greater housing stability. Reforming existing tax benefits, such as the mortgage interest deduction, to better target low- and moderate-income homeowners could also improve affordability for those who can access homeownership . Increasing access to down payment assistance and affordable credit for first-time homebuyers, particularly in historically underserved communities, can help to overcome financial barriers to homeownership for those who lack existing wealth .

Addressing wealth inequality directly can also contribute to improving housing affordability. Implementing taxes on luxury real estate transactions, speculation in the housing market, and vacant properties could generate revenue that can be dedicated to funding the development and preservation of affordable housing . Expanding the social housing sector, which includes community-controlled or publicly owned housing that is outside the speculative market, can provide permanently affordable housing options for low-income individuals and families .

Promoting equitable access to housing is another key policy consideration. This includes implementing and enforcing policies to affirmatively further fair housing and promote housing choice, addressing historical and ongoing discrimination in the housing market . Supporting voucher mobility programs can also enhance the effectiveness of rental assistance by helping families with vouchers move to high-opportunity neighborhoods with better schools and job prospects .

Different Perspectives on Wealth Distribution and Housing Market:

There are varying perspectives on the relationship between homeownership, wealth inequality, and the housing market. Historically, homeownership has been viewed as a significant means for less affluent households to build wealth and achieve financial security . This traditional perspective emphasized the role of homeownership in promoting asset ownership across a wider range of socio-economic groups. However, in recent decades, with rising house prices outpacing income growth, the view has shifted. It is now argued that in the current market conditions, homeownership can actually increase inequality, particularly for those who are unable to access it due to affordability constraints .

Interestingly, cross-country analyses suggest that countries with higher rates of homeownership tend to exhibit lower levels of wealth inequality . This implies that the accessibility of homeownership is a crucial factor. When a large portion of the population can own homes, it can indeed help to distribute wealth more broadly. However, if rising prices and wealth concentration create barriers to homeownership for a significant segment of the population, it can have the opposite effect, exacerbating wealth disparities.

The impact of different asset classes, such as stocks and housing, on wealth inequality also presents varying perspectives. Booming stock markets tend to disproportionately benefit the wealthy, who hold a larger share of corporate equities, while booming housing markets can provide wealth gains for the middle class, who typically have a larger portion of their assets in the form of home equity . This highlights the importance of considering the composition of wealth across different income groups when analyzing the effects of market fluctuations on inequality. The 2008 financial crisis serves as a stark example of how housing market downturns can disproportionately harm the less wealthy, while the subsequent rebound in stock markets primarily benefited those at the top of the wealth distribution, leading to a significant spike in overall wealth inequality .

Finally, it is crucial to acknowledge the persistent racial disparities within the housing market and their contribution to the racial wealth gap. The benefits of homeownership have not been shared equally across racial groups, with significant disparities in homeownership rates, home values, and housing returns . This underscores the need for targeted policies to address historical and ongoing racial discrimination in the housing market to promote equitable wealth-building opportunities and narrow the racial wealth gap.

Conclusion:

The analysis clearly indicates that the increasing concentration of wealth in the United States, particularly the substantial wealth held by the top 1%, is significantly influencing housing affordability and availability for the average buyer. The immense purchasing power of the wealthy, their engagement in housing market investments, and the resulting skewing of development towards luxury properties contribute to higher prices and limited availability of affordable housing options. This situation exacerbates the wealth gap between homeowners and renters and hinders social mobility, creating a cycle of inequality. Addressing this complex issue requires comprehensive policy interventions aimed at both increasing the supply of affordable housing and tackling the underlying wealth inequality. Strategies such as reforming zoning regulations, providing direct funding for affordable housing construction, expanding rental assistance programs, and implementing wealth-based taxes can play a crucial role in creating a more equitable and accessible housing market for all Americans. However, ongoing monitoring and adaptation of these policies will be necessary to navigate the complexities of the housing market and achieve meaningful and lasting change.

----End---

Works cited

1. Share of Net Worth Held by the Top 1% (99th to 100th Wealth Percentiles) (WFRBST01134) | FRED, accessed March 17, 2025, https://fred.stlouisfed.org/series/WFRBST01134

2. Who owns American wealth? - USAFacts, accessed March 17, 2025, https://usafacts.org/articles/who-owns-american-wealth/

3. Wealth inequality in the United States - Wikipedia, accessed March 17, 2025, https://en.wikipedia.org/wiki/Wealth_inequality_in_the_United_States

4. Trends in the Distribution of Family Wealth, 1989 to 2022 | Congressional Budget Office, accessed March 17, 2025, https://www.cbo.gov/publication/60807

5. Trends in the Distribution of Family Wealth, 1989 to 2022 | Congressional Budget Office, accessed March 17, 2025, https://www.cbo.gov/publication/60343

6. Nearly Half of U.S. Households Can't Afford a $250,000 Home | NAHB, accessed March 17, 2025, https://www.nahb.org/blog/2024/05/housing-affordability-pyramid

7. 2024 Housing Market Year In Review: A Tale of Supply, Demand, and Mortgage Rates, accessed March 17, 2025, https://www.redfin.com/blog/housing-market-year-in-review-2024/

8. Economic, Housing and Mortgage Market Outlook – November 2024 | Spotlight: Housing Supply - Freddie Mac, accessed March 17, 2025, https://www.freddiemac.com/research/forecast/20241126-us-economy-remains-resilient-with-strong-q3-growth

9. 2024 U.S. Housing Market Trends: Sales Decline and 2025 Outlook - 208.properties, accessed March 17, 2025, https://208.properties/real-estate-insights/2024-housing-market-trends

10. The Outlook for the U.S. Housing Market in 2025 - J.P. Morgan, accessed March 17, 2025, https://www.jpmorgan.com/insights/global-research/real-estate/us-housing-market-outlook

11. National Comprehensive Housing Market Analysis as of January 1, 2024 - HUD User, accessed March 17, 2025, https://www.huduser.gov/portal/publications/pdf/National-CHMA-24.pdf

12. America's 1 Percent Could Buy Almost Every Home in US, Report Says - Newsweek, accessed March 17, 2025, https://www.newsweek.com/one-percent-could-buy-almost-every-home-us-report-2043340

13. How Billionaire Investors Are Disrupting the U.S. Housing Market - Inequality.org, accessed March 17, 2025, https://inequality.org/article/how-billionaire-investors-are-disrupting-the-u-s-housing-market/

14. Billionaire Blowback on Housing - Institute for Policy Studies, accessed March 17, 2025, https://ips-dc.org/report-billionaire-blowback-on-housing/

15. The effects of income inequality on housing affordability - ScholarWorks, accessed March 17, 2025, https://scholarworks.calstate.edu/concern/theses/5712mf07r

16. Income inequality and housing prices in the very long‐run, accessed March 17, 2025, https://bcec.edu.au/assets/2022/01/Southern-Economic-Journal-88-2021-Hailemariam-Income-inequality-and-housing-prices-in-the-very-long%E2%80%90run.pdf

17. How does the housing market affect wealth inequality? - Economics Observatory, accessed March 17, 2025, https://www.economicsobservatory.com/how-does-the-housing-market-affect-wealth-inequality

18. Interactive: The Unequal States of America | Economic Policy Institute, accessed March 17, 2025, https://www.epi.org/multimedia/unequal-states-of-america/

19. The Wealth Gap between Homeowners and Renters Has Reached a Historic High, accessed March 17, 2025, https://www.urban.org/urban-wire/wealth-gap-between-homeowners-and-renters-has-reached-historic-high

20. Housing Market Appreciation and the White-Black Wealth Gap - Oxford Academic, accessed March 17, 2025, https://academic.oup.com/socpro/advance-article/doi/10.1093/socpro/spae030/7706187

21. wealth and economic mobility | Urban Institute, accessed March 17, 2025, https://www.urban.org/sites/default/files/publication/31206/1001166-wealth-and-economic-mobility.pdf

22. Rebuilding the American Dream: Policy Approaches to Increasing Housing Supply in the U.S. - United States Joint Economic Committee, accessed March 17, 2025, https://www.jec.senate.gov/public/index.cfm/democrats/2024/1/rebuilding-the-american-dream-policy-approaches-to-increasing-housing-supply-in-the-u-s

23. Reducing Housing Burdens While Creating a Longer-Term Affordable Housing Solution, accessed March 17, 2025, https://www.americanprogress.org/article/reducing-housing-burdens-while-creating-a-longer-term-affordable-housing-solution/

24. 5 policy solutions to advance racial equity in housing | Habitat for Humanity, accessed March 17, 2025, https://www.habitat.org/stories/5-policy-solutions-advance-racial-equity-housing

25. The Solution | National Low Income Housing Coalition, accessed March 17, 2025, https://nlihc.org/explore-issues/why-we-care/solution

26. Housing and wealth inequality: A story of policy trade-offs | CEPR, accessed March 17, 2025, https://cepr.org/voxeu/columns/housing-and-wealth-inequality-story-policy-trade-offs

27. Wealth Inequality in America: A Race Between the Stock and the Housing Market, accessed March 17, 2025, https://www.promarket.org/2019/04/29/wealth-inequality-in-america-race-between-the-stock-and-the-housing-market/

28. Racial Differences in Economic Security: Housing | U.S. Department of the Treasury, accessed March 17, 2025, https://home.treasury.gov/news/featured-stories/racial-differences-in-economic-security-housing